A formal Photogrammetry Software Market Competitive Analysis, using the structured framework of Porter's Five Forces, reveals an industry with a unique and challenging competitive structure. The market is defined by an intense technological rivalry among a few key specialists, very high barriers to entry for core processing engines, and a growing threat from substitute technologies and integrated platforms. Understanding these deep structural forces is essential for any company in the space to formulate a sustainable strategy and to appreciate the sources of profitability. The market's explosive growth potential is the primary factor attracting intense competition and investment. The Photogrammetry Software Market size is projected to grow USD 19.54 Billion by 2035, exhibiting a CAGR of 18.2% during the forecast period 2025-2035. A structural analysis shows that while the market is highly attractive, long-term success requires a formidable moat based on either superior technology or deep ecosystem integration to defend against the powerful competitive forces at play.

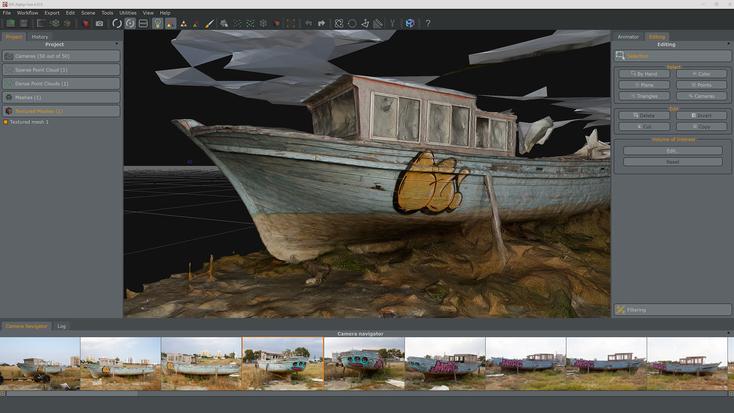

The rivalry among existing competitors is high, but it is primarily a technological arms race between a handful of specialized software providers. Companies like Agisoft, Capturing Reality, and Pix4D compete fiercely on the performance of their core processing engines. This rivalry is based on technical benchmarks: processing speed, the quality of the 3D mesh, and the accuracy of the output. This is a competition of computer vision expertise and algorithmic sophistication. The threat of new entrants at this core engine level is very low. The barriers to entry are immense. It would require a team of world-class PhDs in computer vision and years of dedicated R&D to develop a photogrammetry engine that could compete with the established leaders. The complex mathematics and the closely-guarded intellectual property of the core algorithms create a massive technological barrier that protects the incumbents. However, the threat of new entrants in the application layer—building a new workflow tool on top of an existing engine—is much higher.

The other forces in the model highlight the market's unique pressures. The bargaining power of buyers (the professional users) is moderate. While they have a choice between a few strong competitors, once a professional or a company has invested in a specific software, has trained their staff on it, and has built their workflows around it, the switching costs can be significant. The bargaining power of suppliers is also moderate. The primary "suppliers" are the manufacturers of the drones and cameras that provide the input data. While a software company needs to support the most popular hardware, no single hardware vendor has dominant power over the entire software market. Finally, the threat of substitute products or services is significant and growing. The primary substitute for photogrammetry is LiDAR (Light Detection and Ranging), a different reality capture technology that uses lasers. While more expensive, LiDAR can be more accurate in certain conditions (like in vegetated areas). An even greater substitute threat comes from the major AEC and gaming platforms that are integrating "good enough" photogrammetry capabilities directly into their ecosystems. For a user who only needs a basic 3D model, the convenience of an integrated tool within their primary design software can be a powerful substitute for a dedicated, high-end photogrammetry application.

Top Trending Reports -

US Outsourced Software Testing Market